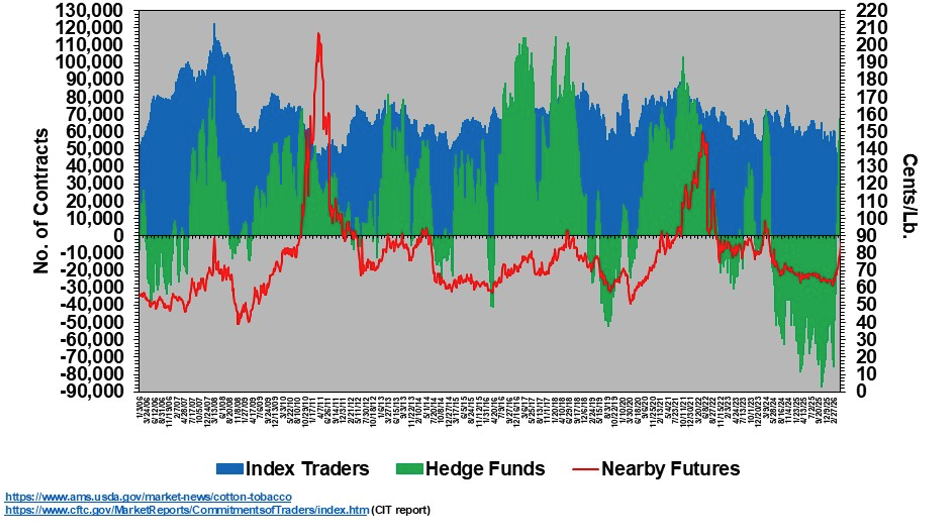

The Commodity Futures Trading Commission (CFTC) publishes weekly “Commitment of Traders” (COT) data on the positions of index funds and hedge funds in agricultural futures markets (Figure 1). The changes in these speculative futures positions have near term value in explaining fluctuations in ICE cotton futures.

For roughly two years, the hedge fund (or “non-commercial” or “managed money”) speculative position has been net short, meaning there is an excess of outright short sellers over longs. This position has been associated with a low level and relatively flat pattern of ICE cotton nearby futures settlements.

In April of 2026, the hedge fund short position in ICE cotton flipped to net long (see the thin upward green spike on the right-hand side of Figure 1). This move was associated with initial buying to cover open short positions, followed by outright new buying. This move is also associated with a twenty-cent rally in nearby ICE cotton futures.

What other market implications are there from this speculative positioning? Judging from the narrowness of many of the green spikes in Figure 1, we observe that the bullish or bearish influence of hedge fund positioning can sometimes be short lived. In the present case, hedge fund buying can act like a catalyst for higher prices, perhaps influencing prices to trend higher and move more quickly than fundamentals might justify. The same can happen in reverse, i.e., liquidation of long speculative positions can contribute to volatility. This has implications for the need for pre-harvest pricing strategies.

The current price outlook for U.S. cotton in 2026 is fundamentally neutral in terms of the year-over-year comparison of ending stocks. The 2026/27 projection of ending stocks is within 500,000 bales of the 2025/26 estimate of ending stocks. But in the near term, speculators and commercials are likely waiting for the unfolding of a so-called “weather market”, i.e., the effect of early dryness and forecasted El Niño moisture on the supply outcome. The hedge funds will play their speculative role in this outcome, and likely contribute to seasonal price volatility.

Figure 1. ICE Cotton Net Position of Index funds and Hedge Funds vs. Nearby ICE Cotton Futures Settlement

January 3, 2006 Through May 12, 2026